Epistemic status: tentative

In the wake of the election, I’ve been thinking about the decline of manufacturing in America.

The conventional story, the one I’d been told by the news, goes as follows. Cheap labor abroad competes with US manufacturing jobs; those jobs aren’t coming back; most manufacturing jobs are lost to robots, not trade, anyhow; this is tragic for factory workers who lose their jobs, and perhaps they should be compensated with more generous social services, but overall the US’s shift towards a service economy is for the best. Opposition to outsourcing, while perhaps an understandable emotional reaction from the hard-hit working class, is simply bad economics. At best, the goal of keeping manufacturing jobs at home is a concession to the dignity and self-image of workers; at worst, it’s wooly-headed socialism or xenophobia.

But what if that story were not true?

Here’s an alternative story, which I think there’s some data to suggest.

Industry — as in, factories in the US making things like cars and trains — is important to long-run technological innovation, because most commercial R&D is in the manufacturing sector, and because factories and research facilities tend to physically co-locate.

High-tech, high-cost-per-unit industries in particular, like the auto industry, are like keystone species in an industrial ecosystem, because you need many different kinds of technology to support them, and because the high cost per unit makes them the first industries where it’s worth it to invest in new process improvements like robotics. If you don’t have heavy industry at home, eventually you won’t have innovation at home.

And if you don’t have innovation at home, your economy may eventually stagnate. Foundational technologies, things like integrated circuits or metallurgy, have high fabricatory depth; better microchips give rise to more computing power which gives rise to untold multitudes of software applications. If your economy lives exclusively on the “leaves” of the tech tree, you aren’t going to be able to capture the value from a long future of continued inventions. There may be high-paying jobs in the service economy, but an entire economy built on services will eventually flatten out.

In other words: maybe industry matters.

And, while industrial jobs may initially leave the US because they’re cheaper elsewhere, foreign labor doesn’t stay cheap forever. As countries industrialize and become wealthier, they gain expertise and advance technologically, and eventually compete on quality, not just on price. Rich countries hope to “move up the value chain”, outsourcing cheap and crude tasks to poorer countries while focusing their own efforts on higher-tech, higher-priced tasks. The problem is that this doesn’t always work — since collocation matters, it may be that you need at least some of the basic factory work to stay at home in order to be able to do the high-tech work, especially in the long run.

“Industry matters”, if true, might be an argument in favor of tariffs, in a vaguely Hamiltonian industrial policy. Now, the laws of economics still hold; tariffs will always cause some degree of damage. I’m not confident that the numbers work out such that even an ideal tariff would be worth it, let alone the trade policy likely to be administered by the actually-existing USG.

“Industry matters” might also be an argument in favor of deregulation designed around making it easier to move around “atoms not just bits.” If environmental and labor regulations make it extremely difficult to build factories in the US, and if industry has an outsized impact on long-run growth, then the cost of regulation is even higher than previously assumed. If a factory doesn’t open, the cost is not only borne by the people today who could have worked in or profited from that factory, but by future generations who won’t be able to work at the new companies which would have been produced from innovations downstream of that factory.

If industry matters, it might be worth it to trade a bit of efficiency today for long-run growth. Not as a concession to Rust Belt voters, but as a genuine value-creating move.

The US is transitioning to a service economy

According to the Bureau of Labor Statistics’ Employment Outlook Handbook, occupations with declining employment include:

- Agricultural workers

- Clerks (file, correspondence, accounting, etc)

- Cooks (fast food and short order)

- Various manufacturing occupations like “machine tool setters” and “electronic equipment assemblers”

- Railroad-related occupations

- Drafters, medical transcriptionists

- Secretaries and administrative assistants

- Broadcasters, editors, reporters, radio and television announcers

- Travel agents

while the jobs with the fastest growth rates include:

- Nurses, home health aides, physician’s assistants, physical therapists

- Financial advisors

- Statisticians, mathematicians

- Wind turbine service technicians, solar photovoltaic installers

- Photogrammetry (i.e. mapping) specialists

- Surgeons, biomedical engineers, nurse midwives, anaesthesiologists, medical sonographers

- Athletic trainers, massage therapists, interpreters, psychological counselors

- Bartenders, restaurant cooks, food preparers, waiters and waitresses

- Cashiers, customer service representatives, hairdressers, childcare workers, teachers

- Carpenters, construction laborers, electricians, rebar workers, masons

Basically, medicine, education, customer service, construction, and the “helping professions” are growing; factory work, farming, and routine office tasks are shrinking, as are industries like news and travel agents that have been disrupted by the internet.

As far as mass layoffs go, in May 2013 the largest sector by number of mass layoffs was manufacturing, where the largest number of people laid off were in “machinery” and “transportation equipment.” Construction followed, where most layoffs were in “heavy and civil engineering” construction.

By sector, mining and manufacturing are losing employment, while construction, leisure and hospitality, education and health, and financial services, are gaining employment.

This part of the conventional story is true: manufacturing jobs really are disappearing.

US manufacturing productivity and output are stagnating

It’s not just jobs, but also productivity and output, where manufacturing in the US is weakening. US manufacturing still produces a lot, but its growth is slowing. We’re not getting better at making things the way we used to.

In the US, the biggest output gains per industry, in billions of dollars, between 2002 and 2012, were in the federal government, healthcare and social assistance, and professional services, at 2.6%, 2.6%, and 2.4% respectively. Manufacturing only grew by 0.2%.

Manufacturing output as a whole between 1997 and 2015 was only growing at 0.8% a year, meaning that it’s slowed down in the last 20 years. Broken down by subsector, the highest manufacturing growth rates were in motor vehicles and other transportation equipment, at an average of about 2% yearly growth; other kinds of manufacturing, such as textiles and apparel, were stagnant or even declined in output. By contrast, the largest output growth between 1997 and 2015 was in information tech, at an average of 5.6% yearly growth, probably coinciding with the rise of the Internet economy.

In other words, US manufacturing isn’t shedding jobs merely because it’s becoming ultra-automated and efficient. US manufacturing growth has slowed down a lot in output as well.

US manufacturing also stagnated in labor productivity and multifactor productivity. Multifactor productivity (the efficiency of labor & capital) in manufacturing has declined at an 0.5% rate from 2007-2014, while it was increasing at a 1.7% rate in 2000-2007, 1.9% in 1995-2000, and 1.1% in 1990-1995. Manufacturing productivity was roughly flat from the 1970’s through 2000.

Manufacturing total factor productivity is still increasing, but has been leveling off.

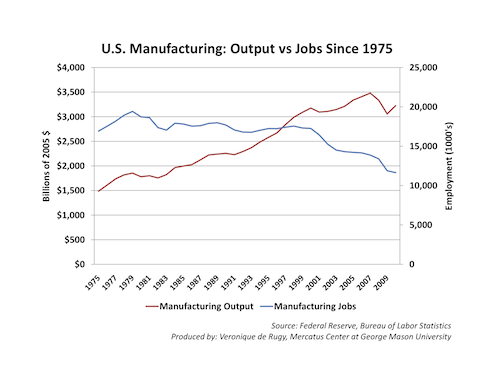

Manufacturing output, similarly, is still increasing, but has been leveling off in recent decades.

While overall manufacturing productivity is still growing over the period 1987-2010, manufacturing output flattened in about 2000.

While manufacturing output seems to have grown roughly steadily since the 1950s, with a slow decline or stagnation in employment from about 1970-2000, note how the output curve seems to be bending at around 2000, just as manufacturing employment plummets.

You can also see this slight bend in the curve, beginning in around 2000, in manufacturing value added.

The story of “we’re getting more efficient and thus using fewer workers” is only part true. We’re getting more efficient, but at a slowing rate. We’re producing more output than we did in the 70’s, but that seems to have leveled off in around 2000. Yes, there’s more output and fewer workers, but it looks like recently, since about 2000, multifactor productivity and output are slowing down.

The Big Three auto manufacturers in the US, between 1987 and 2002, had dropping market share and stock price, largely due to international competition. They lagged the competition in durability and vehicle quality, so were forced to cut prices. They also had a labor productivity disadvantage relative to Japan. It took nearly two decades for US car manufacturers to catch up to Japanese production process improvements.

In other words, the story of the decline in US manufacturing jobs is not merely that we’re a rich country with expensive labor, or a high-tech country that uses automation in place of workers. If that were true, output and productivity would be continuing to grow, and they’re not. US manufacturing is stagnating in quality and efficiency.

Robots aren’t taking American jobs

The decline in US manufacturing began in the 1970’s and 1980’s, as trade liberalization made it easier to move production abroad, and new corporate governance rules made US managers focus on stock prices and short-term performance (which could be boosted by moving factories to cheaper countries.)

Manufacturing automation, by contrast, is much newer, and can’t account for anywhere near that much job loss. There are only 1.6 million industrial robots worldwide, mostly in the auto and electronics industries; an automotive company has 10x the roboticization of the average manufacturing company. That is to say, robots are only being used in the highest-tech sectors of the manufacturing world, and not very widely at that. Industrial robots are a rapidly growing but very recent development; there was a 15% increase in the world’s supply of robots just in 2015.

Moreover, countries with more growth in industrial robotics don’t have more job loss. Most new robots are actually abroad rather than in the US. The largest market is in China, with 27% of global supply; the second largest market is in Europe. The US boosted its purchases of robots by only 5% this year, at well below the global rate of robotics growth.

It is simply false that robots are causing any significant part of US manufacturing unemployment. There aren’t very many, they haven’t been around very long, they’re mostly in other countries, and they don’t hurt employment in those countries.

According to the Bureau of Labor Statistics, no US manufacturing layoffs in 2013 were due to automation.

Most of the news articles about the dangers of technological unemployment are based on projections about which jobs are in principle automatable. This is speculative, and doesn’t take into account new industries that may open up as technology improves (basically the argument from Say’s law.) The “post-work future” is largely science fiction at this point. Lost manufacturing jobs are real — but they weren’t lost to robots.

Trade caused manufacturing job loss

The US-China Relations act in 2000 that normalized trade relations permanently was a “shock” to US manufacturing that US jobs were slow to recover from. Not only did employment plummet, but manufacturing productivity also dropped steeply.

Only 2% of job losses are due to offshoring. But this understates the true amount: if plants close in the US while companies buy from foreign affiliates, that’s effectively “jobs moving overseas” under a different name. Foreign affiliates now make up 37% of the total employees of US multinational companies, a figure that has been steadily rising since the 80’s; it was 26% in 1982.

Moreover, trade can also cause US job losses if foreign-owned companies outcompete US companies. The most common reason given for manufacturing layoffs in 2013 was “business demand”, mostly contract completion. Restructuring and financial problems such as bankruptcy were also common reasons. The main reason for manufacturing layoffs seems to be failure of US factories — poor demand or poor company performance. Some portion of this is probably due to international competition.

In short, it’s freer trade and poor competitiveness on the international market, not automation, that has hurt American manufacturing. It’s not the robots that are the problem — if anything, we don’t have enough robots.

Manufacturing drives the future, and location matters

A McKinsey report on manufacturing notes that while manufacturing is only 16% of US GDP, it’s a full 37% of productivity growth. 77% of commercial research and development comes from manufacturing. Manufacturing, in other words, is where new technology comes from, and new technology drives growth. If you care about the future economy, you care about manufacturing.

R&D, especially later-stage development rather than basic academic research, must be physically proximate to the lead factory even if some production is globalized, for reasons of communication and feedback between research and production. You can’t outsource or trade all your manufacturing without losing your ability to innovate.

Moreover, globalized supply chains have real costs: as trade and outsourcing increase, transportation costs and supply chain risks have also been increasing. Physical proximity places some limits on how widely dispersed manufacturing can be. Trade growth has outpaced infrastructure growth in the US, driving transportation costs up. The cost of freight for steel and iron ore is almost as high as the material itself.

Steel production, in particular, has plummeted in industrialized countries since the 70’s and 80’s, as part of the switch to a service economy. China’s steel and cement production since the 80s seems to have grown rapidly, while its car production seems to be growing roughly linearly. South Korea’s steel production is growing steadily. US car production, by contrast, has been shrinking (in terms of number of units), as has its steel production. Because (due to their weight) metals have unusually high transportation costs, proximity matters an unusual amount, and so a fall in steel production might mean a fall in heavy industry output generally, which is difficult to recover from.

The main theory here is that, once you cease to be an industrial economy, it’s hard to profitably keep factories at home, which means it’s hard to innovate technologically, which means long-run GDP growth is threatened.

The largest manufacturing industries are machines, electronics, and metals

The largest manufacturing companies in China make cars (SAIC, Dongchen, China South Industries Group), chemicals (Sinochem, Chemchina), metals (Minmetals, Hesteel, Shougang, Wuhan), various engineering (Norinco, China Metallurgical group, Sinomach), electronics (Lenovo), phones (Huawei), ships (China Shipbuilding).

The US’s largest manufacturers are general engineering (GE), automotive (GM, Ford), electronics (HP, Apple, IBM, Dell, Intel), pharmaceuticals (Cardinal Health, Pfizer), consumer goods (Procter & Gamble, Johnson&Johnson), aerospace (Boeing, Lockheed Martin), food and beverage (Pepsi, Kraft, Coca-Cola), construction equipment (Caterpillar), and chemicals (Dow).

Germany’s largest manufacturing companies are automotive (Volkswagen, Daimler, BMW), chemicals (BASF), engineering (Siemens, Bosch, Heraeus), steel (ThyssenKrupp), pharmaceuticals (Bayer), and tires (Continental).

Japan’s largest manufacturers are automotive (Toyota, Nissan, Honda), engineering (Hitachi, Panasonic, Toshiba, Mitsubishi, Mitsui, Sumitomo, Denso), electronics (Sony, Fujitsu, Canon), steel (Nippon Steel, JFE), and tires (Bridgestone).

Korea’s largest manufacturers are electronics (Samsung, LG), automotive (Hyundai, Kia), and steel (POSCO).

Machinery and appliances, and electronics and parts, are by far the largest exports from Mexico.

Top exports from China, at a coarse level of granularity, are machines (48%), textiles (11%), and metals (7.8%). At a more granular level, this involves computers, broadcasting equipment, telephones, integrated circuits, and office machine parts.

US‘s top exports are machines (24%), transportation (15%), chemicals (13%), minerals (11%), and instruments (6.3%). More granularly, this is integrated circuits, gas turbines, cars, planes and helicopters, vehicle and aircraft parts, pharmaceuticals, and refined petroleum.

Germany‘s top exports are machines (27%), transportation (23%), chemicals (13%), metals (8.1%), or in more detail: cars, vehicle parts, pharmaceuticals, and a variety of smaller machine things (valves, air pumps, gas turbines, etc).

Japan’s exports are machines (37%), transportation (22%), metals (9.8%), chemicals (8.5%), and instruments (7.8%). Or, in more detail: cars, vehicle parts, integrated circuits, and a variety of machines like industrial printers.

South Korea’s exports are machines (37%), transportation (19%), minerals (8.9%), metals (8.5%), plastics (7.1%). In more detail, integrated circuits, phones, cars, ships, vehicle parts, broadcasting equipment, and petroleum.

“Heavy industry” — that is, machines, engineering, automobiles, electronics, and metals — is the cornerstone of an industrial economy. Integrated circuits are a true “root” of the tech tree, the foundation on which the information economy is built. Capital-intensive heavy industries like automobiles are a “keystone” which is deeply interwoven with the production of machines, parts, robots, electronics, and steel.

It’s a relevant warning sign for Americans that many current developments that seem likely to improve “heavy industry” are not concentrated in the US.

Of the top 5 semiconductor companies, only 2 are American. Some electronics innovations, like flat-screens (developed by Sony) and laser TV’s (developed by LG) were developed by Asian companies, and Mexico is the biggest exporter of flat screen TVs. Robotics, as discussed above, is being pursued much more intensively in Asia and Europe than in the US. “Smart factories”, in which automation, sensors, and QA data analysis are integrated seamlessly, are being pioneered in Germany by Siemens. The majority of drones worldwide are produced by Israel. The Japanese companies Canon and Ricoh, as well as the American HP, are expected to launch 3d printers this year; meanwhile the largest manufacturer of desktop 3d printers, XYZprinting, is Taiwanese.

A positive sign, from a US-centric perspective, is that self-driving cars are being developed by American companies (Tesla and Google.) Another positive sign is that basic research in physics and materials science — the fundamentals that make a continuation of Moore’s law possible — is still quite concentrated in American universities.

But, to have a strong industrial economy, it’s not enough to be good at software and basic research; it remains important to make machines.

Non-xenophobic, economically literate, pro-industry

Globalization has been a humanitarian triumph; Asia’s new prosperity has vastly reduced global poverty in recent decades. To acknowledge that global competition has been hard on Americans doesn’t preclude appreciating that it’s been good for foreigners, and that foreigners have equal moral worth to ourselves.

Acknowledging harms from trade also doesn’t require one to be a fan of planned economies or a believer in a “zero-sum world.” Trade is always locally a win-win; restricting it always has costs. But it may also be true that short-term gains from trade can be counterweighted by long-term losses in productivity, especially due to loss of the gains in local skill and knowledge that come from being a manufacturing center.

If you want to live in a vibrantly growing country, you have to make sure it remains a place where things are made.

That’s not mere protectionism, and it’s certainly not Luddite.

I don’t think this is true of, say, agriculture, where vast increases in efficiency have reduced the number of farmers needed to support the global population, but where that’s not really a problem for overall growth. US farming has not lost ground — we produce more food than ever. We are not getting worse at farming, we just need fewer people to do it. I suspect we are getting worse at manufacturing. And since manufacturing has so disproportionate an effect on downstream growth and innovation, that’s a problem for all of us, in a way that it’s not a problem if farmers or travel agents lose their jobs to new technologies.

Pro-Industry, Anti-Corruption

The truly obvious gains from capitalism are actually gains from industry. Cheap, varied, abundant food. Electricity and electric appliances. Fast transportation. The sort of things described in Landsailor.

Other things that show up in GDP are less obviously good for humans. If real estate prices rise, are we really better housed? If stock prices rise, do we really have more stuff? If we spend more on medicine and education but don’t have better health outcomes or educational outcomes, are we really better cared for and better educated?

The value of firms has dramatically shifted, since 1975, towards the “dark matter” of intangibles — things like brands, customer goodwill, regulatory favoritism, company culture, and other things that can’t be easily measured or copied. US S&P 500 firms are now 5/6’ths dark matter. How much of the growth in their value really corresponds to getting better at making stuff? And how much of it is something more like “accounting formalism” or “corruption”?

If you are suspicious of things that cost more money but don’t create obvious Good Things for humans, then you will not consider a shift to a service economy a good outcome, even if formally it doesn’t look too bad in GDP terms. If you take a jaundiced view of medicine, education, the “helping” professions, government, and management — if you see them as frequently doing expensive but unhelpful things — then it is not good news if these sectors grow while manufacturing declines.

If your ideal vision of the future is a science-fiction one, where we cure new diseases, find new fuel sources, and colonize the solar system, then manufacturing is really important.

The old slogans like “what’s good for GM is good for America” are not as far from the truth as you’d think.

It doesn’t matter where the innovation happen as long as you can buy the product of said innovations. The best way to do that is for them to happen where it’s cheapest to make things, and for you to do what you are comparatively best at so you have things to trade for said new things.

The innovations might not happen in America, but why does that matter as long as they happen? The answer seems to be nationalism.

It doesn’t matter where the innovation happen as long as you can buy the product of said innovations. The best way to do that is for them to happen where it’s cheapest to make things, and for you to do what you are comparatively best at so you have things to trade for said new things.

The innovations might not happen in America, but why does that matter as long as they happen? The answer seems to be nationalism.

Recommenting logged in with my new WordPress account, so I can get notifications without having to get emails.

I think you misunderstand.

First of all, I’m talking here about American wellbeing, so this essay is America-centric in that respect. But that’s just because I live here. I think it would make perfect sense for a Chinese version of me to write an essay about Chinese long-run well-being. I’m only “nationalist” in the sense of caring about the interests of the place where I live.

You seem to be saying that it “doesn’t matter where innovation happens” — that Americans will be just as well off if they import things as if they produce them. I think this is not quite true. For at least a while after a commercial invention occurs, monopoly power (or monopolistic competition) means that the people involved in making it can capture value. If someone founds Apple, an outsize portion of the gains go to Apple stockholders and employees. Because transaction costs are a thing, a fair chunk of the people who gain from innovative monopolies are in the same country. The creation of Apple is a good thing for everyone in the world, consumers as well as producers/owners, but the latter *do* get an extra chunk of value because Apple products are not commodities. The advantage of innovating at home is getting that extra, monopolistic value.

I think it’s pretty clear that total growth does not depend on where innovations happen very much, conditional on their happening and bring implemented.

Americans might not be as well off if the innovations happen in China and we buy them versus their happening here (if that could happen magically without paying whatever costs made it happen in China in the first place), but then China and it’s people will be richer than if they happen here so it washes out. Overall it doesn’t really matter. Unless you think Americans or America as a location or culture are uniquely innovative or something in a way Chinese people or China can’t match, but that seems unlikely.

Since trade policies to favor yourself cause the whole world to get poorer in the short term, and are risky (they threaten trade wars and depressions), the rational response would be a program Thiel would like of eliminating regulations (since that increases wealth even in the short term while helping your competitiveness long run). Going beyond that requires entering the world of zero sum games where you country has to win and others lose. Generally those lead to everyone being worse off.

I like deregulation better than tariffs or subsidies (unsurprisingly, if you know me!)

By “total” growth do you mean global growth? That’s what seems to be implied by “but then China and it’s people will be richer than if they happen here so it washes out”.

Yes, global growth, total human prosperity.

ah. yes. you’re less nationalist than me (at least, less than I’m being in that post.) From a global perspective, it’s all good, doesn’t matter where things are.

I love this piece. THIS is the important issue which defines recent politics above all. This is what we have to address not just to win but because it’s good for us and for others.

A company of a hundred people can be automated into ten without any physical robots – with twenty year old computer technologies that still haven’t been effectively adopted by modern firms. Many companies could be revolutionized by learning how to use an excel spreadsheet properly. Process improvements, communication improvements, training improvements – and the fact that so much work which used to be manual is done automatically behind the scenes by a database server.

From my perspective almost everything I can think of which matters to me has gotten better by such a massive margin that I can’t possibly expect a higher growth rate. Still, just as medical outcomes for me are ten times better because I can access the information online even if others don’t – many of the developments I value most are ones few people even know how to apply. I feel that the power of tech and tech integration has far outpassed human capability to take advantage of it, and that we as a culture are still trying to figure out how to fully integrate the advances of thirty years ago.

What if the job loss isn’t in manufacturing, it’s in book-keeping? What if we don’t see the invisible benefits of a thousand unpaid accountants now deliverable in the size of a rasberry PI – are these properly counted in GDP? And what if manufacturing is being held back primarily because of a lack of demand at the price possible given physical resource limitations and transportation costs?

I’m trying to reconcile this piece: http://www.themoneyillusion.com/?p=31847

“Back in 1967, the US steel industry employed about 780,000 workers, and produced about 115 million tons of steel. By 2015, employment had fallen to 90,000, producing about 79 million tons of steel. In both years the US consumed about 130 million tons of steel. (I’m not sure these figures are exactly right, but I think they are close enough.)”

with the claim that manufacturing efficiency has not increased. Are Scott Sumner’s figures straight up wrong? Which source is correct- that we are making 68% the steel with only the 11% the workers, or that productivity increase has been approximately flatlined? I can see individuals, even those who are unmotivated, untrainted, and unsuited – doing work which in the past would have been the domain of Hercules – I cannot help but feel that should be showing up in the numbers.

Manufacturing efficiency has improved since the 70’s, just at a low and declining rate.

But I haven’t cross-checked the numbers directly yet.

Another thought: if modern technology and automation (of the computerized style) is massively boosting productivity in fields which *aren’t* manufacturing it is a relative advantage for a nation which can take most advantage of tech to avoid manufacturing when possible.

Tesla and iPhone are not being designed in China, even if the physical manufacturing is outsourced to that location. How critical is the supply chain to innovation – why are there so few globally dominating products from powerhouse manufacturing countries?

Another thought – might the supply chain issue resolve itself if it becomes a real problem for market leading US firms? If costs and time delay from transportation are high enough they should start paying more, much more, for US-based companies to do this work – albeit with a lag time.

My feeling is that what people want they’re not getting are not primarily manufactured goods but rather rivalrous goods – housing, the best doctors and lawyers, the best schools. And I’m not sure how that *can* be provided regardless of tech advancement without redefining methods and expectations socially.

Ok, more serious reply. The numbers linked at that blog imply an average annual 3.8% growth in the labor productivity of steel, from 1967 to 2015. According to the BLS, average annual percent change in labor productivity in “Iron and steel mills and ferroalloys” from 1987 to 2014 has also been 3.8%. (http://www.bls.gov/news.release/pdf/prin.pdf) 3.8% per year productivity improvement is a whole lot. This looks like a closer match to the story of “labor productivity went up and cost jobs” than manufacturing as a whole.

However it still seems relevant that US steel production went down in around 1980 and stayed down to the present day. (see http://www.tradingeconomics.com/united-states/steel-production). We got more efficient at making steel, yes, but we also just made less of it, period. The job loss, in other words, was not wholly due to productivity improvement, it was just exacerbated by it.

The US also has an unusually high corporate tax rate.

https://en.wikipedia.org/wiki/Corporate_tax_in_the_United_States

Not just corporate: Personal too. This, along with several current problems with current patent law, strongly discourage innovation from lone inventors as well as from bigger companies.

Corporate tax rate as implemented in the US seems mostly likely to lead to weird distortions in how international corps doing business in the US are structured, not to especially penalize manufacturing over other things.

An example of a tax likely to encourage some industries over others is Washington State’s tax on gross receipts (http://dor.wa.gov/content/findtaxesandrates/bandotax/ ). Since it’s not an income tax, it discourages low-margin businesses (such as manufacturing goods low on the value chain, McDonald’s, anything else highly competitive) and encourages high-margin ones (new products, monopolies, rent-seeky professional firms mostly selling services).

The McKinsey report just says manufacturing contributes to 37% of productivity growth, not GDP growth, as far as I can tell. Not sure how to interpret either of these – though basically it suggests that manufacturing’s getting more efficient – producing higher-value things with cheaper inputs, e.g. less employment per unit of output.

The graph of manufacturing output vs manufacturing employment seems to suggest that the “manufacturing is stagnating” story is false; it looks like real manufacturing output increased pretty steadily from about $300 billion in 1947 to about $1,800 billion in 2010, about 6x growth over 63 years. That’s a little under 3% growth annually, somewhat lower than overall real US GDP growth for the period but higher than recent GDP growth. From visual inspection it doesn’t look like the graph meaningfully deviates from the trend; remember that 2002-2012 includes the Great Recession, in which we should expect industries not propped up by government spending to decline relative to trend, so the 0.1% number isn’t all that troubling to me.

Overall this seems broadly consistent with the US moving up the value chain and getting more efficient, not a secular decline in manufacturing capacity per se. Trade leads to reduced manufacturing in areas where US companies don’t have a special advantage, but this is compensated for by higher-value manufacturing.

What am I missing?

>The truly obvious gains from capitalism are actually gains from industry. Cheap, varied, abundant food. Electricity and electric appliances. Fast transportation. The sort of things described in Landsailor.

>Other things that show up in GDP are less obviously good for humans. If real estate prices rise, are we really better housed? If stock prices rise, do we really have more stuff? If we spend more on medicine and education but don’t have better health outcomes or educational outcomes, are we really better cared for and better educated?

I think this misses gains from *trade*, and gains from making the right things and not the wrong things, and getting things to the right market where people actually want them. The parody of Communism in which the factory incentivized by weight of nails produced makes one giant nail never actually happened because people have common sense, but there’s a less funny central-planning problem where we have lots of CAT scans and antibiotics and psychiatrists and nuclear reactors, and too few implantable contact lenses with heads-up displays and solar panels and self-driving cars and community leaders. The value of industrial policy depends very heavily on getting the right answer in terms of picking a winner, and the other side can always do the same thing, leading to overall overinvestment anyway.

Good point. “More” investment in industry is not necessarily good & central planning has huge risks of picking the wrong “winners.”

I agree with this. I feel that GDP does a really bad job of encompassing quality of life improvements from doing things better, and this hits at a key reason or side of that I just couldn’t find. Modern tech is giving me *so much* I (would) pay a lot for but is just free. The value isn’t being counted because it’s so cheap to produce.

The McKinsey report was a typo, now fixed.

I added some additional graphs on overall manufacturing output and productivity. The trend is still positive, but since 2000 there seems to have been a leveling out in output and productivity (corresponding to a big drop in employment.) Maybe you think this is too recent to constitute a trend, but I suspect it’s a thing. And it preceded the Great Recession. I miswrote/was unclear about “secular decline in manufacturing capacity.” I don’t think it’s declining, I think it’s increasing at a decreasing rate. (Which weakens but doesn’t destroy my main overall point.)

So the incentives that matter are the ones affecting whether or not your smartest people are working on manufacturing innovation or things upstream from manufacturing innovation (physics, chem, materials science). My frame for this is that better and cheaper physical methods improve the testbed for experiments and thus shorten the feedback loop on innovation. Tighter feedback loops allow for measurable expertise to be developed, and more scalable cross pollination from more repeatable results (cheaper = more people have it and can remix your results more easily).

So the overall story is something like there is a pipeline running from the scientific method on one end to innovations that affect near mode things on the other. Manufacturing methods, in this story, is a non-obvious bottleneck along this pipeline.

(not that this is original reasoning, just useful to try to codify it for efficient use in other models)

by “non-obvious” do you mean you’re skeptical that it’s a bottleneck, or that it *is* a bottleneck but that this isn’t obvious?

Struggling to come up with words that capture it. Something like, it is useful to regard 2nd order effects here as being distinct from the way manufacturing is normally regarded as a bottleneck. So I want to do the pink-purple ball thing on this post (or this aspect of this post) so I can reference it more cheaply when trying to think about it.

There’s also some piece of it around well functioning feedback loops being mostly domain specific which means you don’t get them for free (see Hanson’s recent post on the final step in the innovation pipeline failing in organizational innovation). This might be part of what tends to break over time, eg it was being sheparded by a particular person who can’t really explicitly teach it (procedural knowledge of many small failures).

Manufacturing methods, in this story, is a non-obvious bottleneck along this pipeline.

“The sort of creativity that led to spurts in economic and social progress comprised insights that were motivated by perceived need and by institutional incentives, and could be achieved by drawing on practical abilities or informal education and skills. Elites and allegedly “upper-tail knowledge” were neither necessary nor sufficient for technological productivity and economic progress.”

“However, for developing countries with scarce human capital resources, such inputs at the frontier of “high technology” might be less relevant than the ability to make incremental adjustments that can transform existing technologies into inventions that are appropriate for general domestic conditions.”

From “Knowledge, Human Capital and Economic Development: Evidence from the British Industrial Revolution, 1750-1930″

linky: http://www.overcomingbias.com/2016/11/needed-social-innovation-adaptation.html

Ah, the thought I was trying to think. Manufacturing is normally thought of as downstream from scientific innovation, but it runs both ways. This falls under: if a model is actually important check for reverse causality, lest you accidentally cargo cult.

A related book: https://www.amazon.com/Producing-Prosperity-America-Manufacturing-Renaissance/dp/1422162680/

“For years—even decades—in response to intensifying global competition, companies decided to outsource their manufacturing operations in order to reduce costs. But we are now seeing the alarming long-term effect of those choices: in many cases, once manufacturing capabilities go away, so does much of the ability to innovate and compete. Manufacturing, it turns out, really matters in an innovation-driven economy.”

Related https://www.technologyreview.com/s/426423/standing-up-for-manufacturing/

http://conexus.cberdata.org/files/MfgReality.pdf estimates that only 13% of manufacturing job losses 2000-2010 were due to trade, with the rest due to productivity increases. Do you disagree with their methodology?

This paper estimates that only 13% of manufacturing job losses 2000-2010 were due to trade, with the rest due to increased productivity. They seem to be using different productivity measures than you are. Do you disagree with their methodology?

I’ve been seeing similar numbers from a lot of studies. I am less confident of my original thesis than I was when I wrote this post, and may have to wind up reversing my position.